Impractical to assume sales mix remain constant since this depends on the changing demand levels. CVP simplifies the computation of breakeven in break-even analysis, and more generally allows simple computation of target income sales. It simplifies analysis of short run trade-offs in operational decisions. Cost–volume–profit (CVP), in managerial economics, is a form of cost accounting.

The Guide to Financial Modeling and Forecasting

However, a major disadvantage is that the graph does not clearly reveal how costs vary with changes in activity. An advantage of the P/ V graph is that profits and losses at any point in time can be read directly from the vertical scale. An advantage of the P/V graph is that profit and losses at any point can be read directly from the vertical axis. You now know about CVP analysis and its components, as well as the assumptions and limitations of this method. You also know how to use Google Sheets to carry out your own CVP analysis.

Chapter 15 – Cost-volume Profit (CVP) Analysis and Break-Even Point

The decision maker could then compare the product’s sales projections to the target sales volume to see if it is worth manufacturing. Cost categories that are typically included in a CVP analysis include fixed costs, variable costs, direct materials, direct labor, and overhead expenses. These costs can be identified through an organization’s income statement or accounting records.

What are the weaknesses of CVP analysis?

An organization may use CVP analysis as a planning tool when the management wants to find out the desired profit when the sales volume is known. Break-even analysis is a tool that can be used to demonstrate and calculate how much revenue is needed to make a certain amount of profit, assuming expenses remain constant. You can evaluate different strategies using what-if analysis and setting a profit target.

Example of Cost Volume Profit Analysis

Break-even point is the level at which total revenue equals total costs, i.e. when a company or organization makes neither a profit nor loss. In summary, fixed costs are costs that remain constant regardless of the volume of sales or production. Identifying fixed costs is important for understanding a company’s profitability and cash flow, making informed decisions, and budgeting and forecasting. CVP analysis, in short, enables establishing relationship between cost, volume of products, and profit margin. Managers must monitor a company’s sales volume to track whether it is sufficient to cover, and hopefully exceed, fixed costs for a period, such as a month. Contribution margin is useful in determining how much of the dollar sales amount is available to apply toward paying fixed costs during the period.

Cost-volume-profit (CVP) analysis

- If the company sells less than 2,000 widgets, it will incur a loss; if it sells more than 2,000 widgets, it will profit.

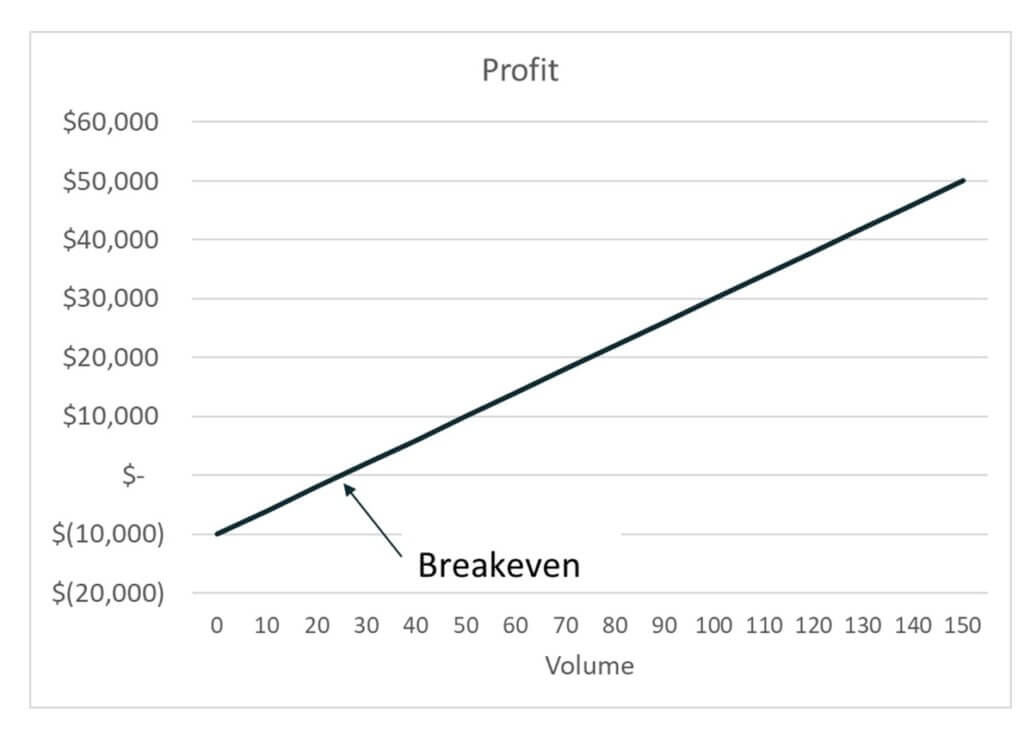

- The point where the total costs line crosses the total sales line represents the break-even point.

- In summary, the break-even point is the level of sales at which a company’s total revenues are equal to its total costs, resulting in neither a profit nor a loss.

- Because they were small, the company could not charge enough to cover its costs.

- On the X-axis is “the level of activity” (for instance, the number of units).

It involves identifying fixed and variable costs, determining the break-even point, and analyzing how changes in volume impact profits. It provides valuable insights into the financial dynamics of a business. CVP analysis is used to determine whether there is an economic justification for a product to be manufactured.

While this may or may not be true in the short term, it’s very unlikely to remain true for longer timespans. For this reason, this analysis is more effective when evaluating short-term decisions. If the store sells $30,000 worth of merchandise monthly, the variable costs may increase to $15,000.

One can think of contribution as “the marginal contribution of a unit to the profit”, or “contribution towards offsetting fixed costs”. The point where the total costs line crosses the total sales line represents the break-even point. This is the point of production where sales revenue will cover production costs. For our sub-business, the contribution margin ratio is ⅖, or 40 cents of each dollar contributes to fixed costs. With $20,000 fixed costs/divided by the contribution margin ratio (.4), we arrive at $50,000 in sales. Cost Volume Profit (CVP) Analysis is a technique used to determine the volume of activity or sales required for an organization to break even or make a profit.

It looks at the relationship between costs, sales volume, and profits over various levels of activity. However, the graph can be interpreted only within the relevant range of operations (i.e., the level of activity over which fixed costs are assumed to remain fixed). To learn more about this, check out our related articles on Break-Even Analysis, How To Find Variable Cost, and How To Find Fixed Cost. Semi-variable or semi-fixed costs are particularly tricky to break down, as the proportion of fixed and variable costs can also change.

Costs, the first component, represent the expenditures incurred by a business in its operations. Fixed costs remain constant regardless of production levels, whereas variable costs fluctuate with the production volume. In summary, the contribution margin is the amount of revenue left over after variable costs have been deducted from the sales price of a product. It is an important concept in Cost-Volume-Profit (CVP) analysis and can help businesses make informed decisions about pricing, product mix, and resource allocation.

Thisremainder contributes to the coverage of fixed costs and to netincome. In Video Production’s income statement, the $ 48,000contribution margin covers the $ 40,000 fixed costs and leaves $8,000 in net income. A cost-volume-profit chart is agraph turbotax troubleshooting that shows the relationships among sales, costs, volume, andprofit. The illustration shows acost-volume-profit chart for Video Productions, a company thatproduces DVDs. The variable cost per DVD is$12, and the fixed costs per month are $ 40,000.